Your gross monthly earnings is the total amount of pre-tax earnings you earn each month. Whether you should include anybody else's income in this computation depends upon who's going to be on the loan. If somebody else is using with you, then you must factor their earnings, in addition to their financial obligations, to the calculation.

The resulting quotient will be a decimal. To see your DTI portion, increase that by 100. In this example, let's state that your month-to-month gross household earnings is $3,000. Divide $900 by $3,000 to get. 30, then multiply that by 100 to get 30. This implies your DTI is 30%.

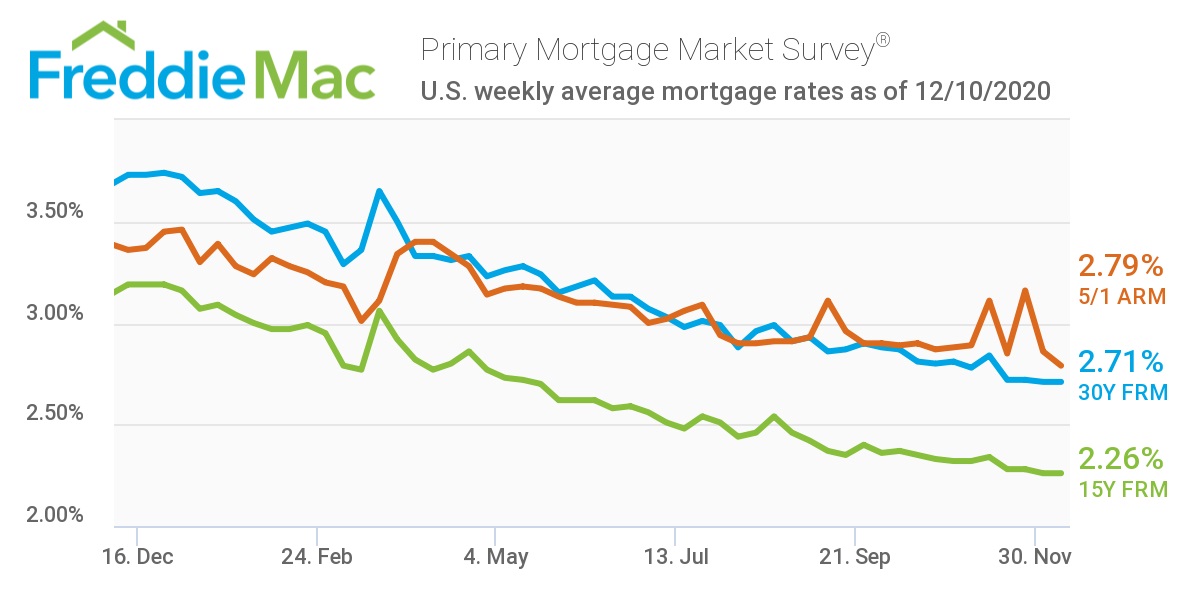

- Over 6 million households did not make their lease or mortgage payments and 26 million individuals missed their trainee loan payment in September, according to third-quarter 2020 research released today by the Mortgage Bankers Association's (MBA) Research Institute for Housing America (RIHA). The new findings provide fresh insights to RIHA's study, Housing-Related Financial Distress Throughout the Pandemic, which was very first released in September. Mortgage are normally structured as long-term loans, the regular payments for which are similar to an annuity and calculated according to the time value of cash solutions. The most fundamental plan would need a fixed monthly payment over a duration of 10 to thirty years, depending upon local conditions.

4 Easy Facts About What Is The Current % Rate For Home Mortgages? Shown

In practice, many variants are possible and typical around the world and within each nation. Lenders supply funds against property to earn interest earnings, and typically borrow these funds themselves (for instance, by taking deposits or providing bonds). The cost at which the loan providers borrow money, therefore, affects the cost of borrowing.

Mortgage lending will likewise consider the (perceived) riskiness of the mortgage, that is, the probability that the funds will be paid back (usually thought about a function of the creditworthiness of the debtor); that if they are not paid back, the loan provider will have the ability to foreclose on the realty bluegreen timeshare cancellation assets; and the financial, rate of interest danger and dead time that might be associated with certain circumstances.

An appraisal might be purchased. The underwriting procedure might take a couple of days to a few weeks. Often the underwriting process takes so long that the provided monetary declarations need to be resubmitted so they are present. It is suggested to maintain the very same work and not to utilize or open brand-new credit throughout the underwriting process.

How What Beyoncé And These Billionaires Have In Common: Massive Mortgages can Save You Time, Stress, and Money.

There are numerous types of home loans used worldwide, but a number of factors broadly specify the qualities of the mortgage. All of these might go through regional regulation and legal requirements. Interest: Interest may be fixed for the life of the loan or variable, and modification at certain pre-defined periods; the interest rate can likewise, of course, be higher or lower.

Some home loan loans might have no amortization, or need full payment of any remaining balance at a particular date, http://edwinmzgb002.bravesites.com/entries/general/some-known-details-about-how-do-reverse-mortgages-work or perhaps unfavorable amortization. Payment amount and frequency: The amount paid per period and the frequency of payments; in many cases, the amount paid per period may alter or the debtor might have the choice to increase or reduce the quantity paid.

The 2 fundamental kinds of amortized loans are the fixed rate home mortgage (FRM) and adjustable-rate home mortgage (ARM) (also called a floating rate or variable rate home mortgage). In some countries, such as the United States, repaired rate home mortgages are the norm, but floating rate mortgages are relatively common. Combinations of repaired and drifting rate home mortgages are also common, where a mortgage loan will have a fixed rate for some period, for instance the first five years, and differ after completion of that period.

The Single Strategy To Use For When Did Subprime Mortgages Start In 2005

In the case of an annuity payment scheme, the periodic payment remains the same quantity throughout the loan. When it comes to linear repayment, the routine payment will gradually decrease. In an adjustable-rate mortgage, the rates of interest is generally fixed for a time period, after which it will regularly (for instance, yearly or monthly) adjust up or down to some market index.

Considering that the threat is transferred to the debtor, the preliminary interest rate might be, for example, 0. 5% to 2% lower than the average 30-year fixed rate; the size of the price poconos timeshare promotions differential will be related to debt market conditions, consisting of the yield curve. The charge to the debtor relies on the credit risk in addition to the rate of interest danger.

Jumbo home loans and subprime financing are not supported by federal government assurances and face greater interest rates. Other innovations explained below can affect the rates also. Upon making a mortgage loan for the purchase of a residential or commercial property, loan providers usually require that the debtor make a down payment; that is, contribute a portion of the cost of the home.

Not known Details About How Much Is Tax On Debt Forgiveness Mortgages

The loan to worth ratio (or LTV) is the size of the loan versus the worth of the property. For that reason, a home mortgage loan in which the purchaser has actually made a deposit of 20% has a loan to worth ratio of 80%. For loans made against homes that the borrower currently owns, the loan to worth ratio will be imputed against the estimated value of the residential or commercial property.

Given that the worth of the property is an essential consider comprehending the threat of the loan, figuring out the worth is a crucial element in home mortgage lending. The value may be determined in different methods, however the most typical are: Actual or deal worth: this is usually taken to be the purchase rate of the home.

Evaluated or surveyed value: in a lot of jurisdictions, some form of appraisal of the value by a certified specialist prevails. There is frequently a requirement for the lending institution to obtain an official appraisal. on average how much money do people borrow with mortgages ?. Estimated worth: loan providers or other celebrations may utilize their own internal estimates, particularly in jurisdictions where no official appraisal treatment exists, but likewise in some other circumstances.

Getting The Who Provides Most Mortgages In 42211 To Work

Common denominators include payment to earnings (home mortgage payments as a portion of gross or net income); debt to income (all debt payments, including home loan payments, as a percentage of income); and various net worth measures. In numerous countries, credit ratings are used in lieu of or to supplement these steps.

the specifics will vary from location to area - which mortgages have the hifhest right to payment'. Income tax rewards typically can be used in kinds of tax refunds or tax reduction plans. The first suggests that earnings tax paid by private taxpayers will be refunded to the extent of interest on mortgage required to acquire residential property.

Some loan providers may also need a potential debtor have several months of "reserve assets" offered. To put it simply, the borrower might be needed to reveal the availability of sufficient properties to spend for the housing costs (consisting of home mortgage, taxes, and so on) for a time period in the event of the task loss or other loss of income.